admin

Comments

-

This is due to the law of large numbers. https://en.wikipedia.org/wiki/Law_of_large_numbers

A 6-month policy and a 12-month policy may have the s…

-

Hi,

To prove the CDF for the diminishing deductible you should think about the various payout intervals and apply conditional probability to ensure summing to 1.

I'll show the second case, where the payout, x, comes from a loss that r…

-

I think this question is okay where it is because it should be taken in the context of parts d and e which are about deductibles. Calculating a guaranteed cost premium is something the CAS assumes you know how to do by the time you reach exam 8. …

-

Okay, based on your feedback we've added all of the Battlecards to the Full BattleQuizzes. The ones that previously weren't showing are now labeled with Qz-10.

We'll keep it this way for at least the rest of this sitting and welcome everyo…

-

Thanks for the feedback, at the moment the Full BattleQuiz feature for Exam 8 groups of all the mini BattleQuizzes within a wiki article. We're trying to keep the volume of questions within each mini BattleQuiz to a reasonable number to balance f…

-

The primary loss pick is the insured's estimate of the largest per-occurrence loss on a policy. When pricing a policy with both a per-occurrence and an aggregate limit we form the entry ratio by taking the ratio of the policy aggregate limit divi…

-

Hi,

It's important to remember whose perspective we're rating from and what data is available. We're rating using the reinsurer perspective using data from the primary insurer. So the subject premium is GNEPI (or GNWPI), i.e. the primary in…

-

Hi,

In both cases the reinsurer expected loss and ALAE is determined by: exposure factor * (expected loss and ALAE ratio) * subject earned premium.

Where differences arise is how you calculate the ground-up expected loss and ALAE rati…

-

Under the "Policy Characteristics" we're told there is a per-occurrence limit and an aggregate deductible. This means we need to price using either the Limited Table M approach or Table L approach.

Generally speaking you can choose which m…

-

Great question and comment thank you. Remember, a rectangle is a special case of a trapezoid where the two parallel sides have equal length.

Also recall the vertical slicing method gets the exact answer because it forces you to consider ev…

-

This is a good example of the CAS writing a question where they intended candidates to answer in a particular way but left a shortcut available.

Yes, Model 1 is equivalent to Model 2. However, note you must have a balanced retrospective rat…

-

Hi,

We prefer to leave our Excel files protected as one of the benefits is it more closely reflects the Pearson VUE exam environment. We want our users to feel at ease within the Pearson environment on exam day.

We are not attempting …

-

Great question and it really depends on the context. In general it's appropriate to roll into the base level so if "trucks" are being eliminated and "cars" is the base level then you could recode all trucks to read "cars" and proceed. Or you coul…

-

We're given information about an industry experience rating plan, i.e. one that could be adopted by many insurers in the market place.

First we need to explain how the incorrect credibilities impact both large and …

-

This is a good example of the CAS making an easy question challenging through burying the important details in words.

We're given claim frequencies for "bodily injury liability coverage" which implies the insured has a current auto…

-

Yes, that's the case. Retrospective rating without any limits allows the insurer to potentially bill or reimburse large amounts of premium depending on if the insured has poor or good experience. By including a per-occurrence limit or deductible …

-

It's helpful to think about who is paying for the losses in this situation.

An LDD plan has the insurer paying the losses above the deductible and seeking reimbursement for the deductible losses from the insured. A retro plan has the insure…

-

You are correct. With the change in how the NCCI produces its retrospective rates (now using the NCCI Circular) we aren't given enough information in this problem to find psi(r_G) and psi(r_H). That's why we added the values used in the examiner'…

-

The question is still valid I'm afraid. It's a good application of the balance equations.

The figures you're asking about are the result of switching from working with entry ratios to working with loss ratios. Notice 1.65 = 165% which is th…

-

Here's the general philosophy I use with this type of pricing:

- Who pays what? For example, does the insurer pay everything and then seek recovery? If there's the potential to recover then we have credit risk.

- Who is doing the s…

-

Splitting hairs here. You're correct that the order (or degree) of a polynomial refers to its highest power. However, by referring to a polynomial we're implicitly allowing all lower order terms to be included else we would refer to the monomial …

-

This is another great example of the CAS regularly changing the syllabus readings so they no longer match the past exam papers they've released.

According to the Fisher reading in the 2021 syllabus, the basic premium includes both the expec…

-

An nth degree polynomial is of the form a_0 + a_1*x + a_2*x^2 + ... + a_n*x^n. So a second degree polynomial requires 3 coefficients. However, we only gain two additional degrees of freedom because we already have an intercept term in the GLM. Th…

-

I think the graders would penalize you for using VAR.S() if the question is worth a significant amount of points and there's clearly non-uniform weights such as manual premium or TT counts etc. Otherwise, I think it would be okay…

-

Great question - the sample answer is definitely scant on some pretty important points.

I'll assume you're fine with part a.

You are correct that there aren't handy equations for getting the maximum and minimum premiums (G and H). The…

-

We reviewed the NCCI circular extract provided in the study kit and this is how they presented it. That said, we definitely share your concern about potentially double counting LAE. We think it is okay and that the excess loss factor loss adjustm…

-

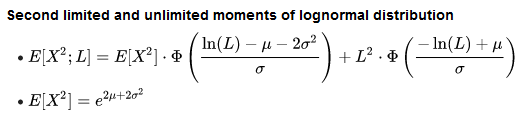

Bahnemann Section 2.4 (p. 53) provides these formula. I've put them below for your convenience.

I believe this is a matter of presentation rather than substance because we're used to thinking about the size of losses and how they change, but we're not as used to thinking in terms of changes in the cumulative distribution. It's rather like w…

{kind=link}