2012Q5

Hi there,

For Part (b), the solution calculates PT relative to TT as (pure premium relativity for HG) * (credibility relativity from multi-dimensional).

Could you please explain what do those "Predicted" relativity under multi-dimensional output actually mean, and ultimately why do we need to multiply by the (pure prem relativity for HG) instead of just using the credibility relativity from multi-dimensional?

- Are those the relativity to TT or relativity to HG?

- Are these relativities the output from the whole "Credibility Considerations" section in the Battlewiki, i.e. calculating the EPV, VHM, variance, covariance matrix etc?

- Why do we need to multiply by the (pure prem relativity for HG) instead of just using the credibility relativity from multi-dimensional? Is it because the sample means are normalized within the HG? What if the sample means are not normalized within HG, can we just directly use the credibility relativity from multi-dimensional "Predicted"?

Thanks.

Comments

TT claims are used as the exposure base for the lower frequency, higher severity injury types. Frequency is measured by per $100 of payroll and severity backed into. All raw frequencies and severities by injury type are converted into relativities to the TT frequency (severity). Then the multi-dimensional credibility process is applied to predict for each class within the hazard group by injury type. The output is aggregated into quintiles by the volume of TT claims and weighted averages calculated. The data is then normalized so we can compare across methods using the sums of squared errors. All of this is already summarized in the question for you so you don't have to perform the calculations.

Classes are grouped into hazard groups because the individual class experience is too volatile. We can calculate the frequency and severity for the TT claims within a hazard group. For the other claim types we can calculate their frequency and severity for the hazard group relative to the TT claims so we can use the TT claims as an exposure base.

Then we have three options available to us.

In options 2 and 3, if we don't normalize so that the hazard group is 1.000 overall then we'll either overstate or understate the class's pure premium relative to TT claims.

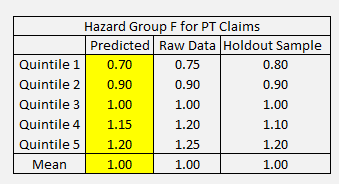

In part (a), why was the SSE calculation for raw to holdout not required for full credit?

I think the CAS examiner's report is sloppy here. I agree with you, to guarantee full credit in the future you should check whether the SSE is lowest for the raw data or justify why you don't need to.

If I had to guess, I'd say the CAS thought people would look at the predicted and raw data and notice they are the same values except for quintile 1 (0.75 / 0.70) and quintile 5 (1.25 / 1.30).

In both quintiles 1 and 5, the raw data is further away from the holdout sample than the predicted value is. Therefore, without calculation we know the SSE for the raw data is higher than the SSE for the predicted data. So to choose whether to or not to use the multi-dimensional credibility it's enough to see if the multi-dimensional SSE is lower than the predicted SSE. It would have been nice if the examiner's report stated that observation.